यह भी देखें

08.11.2024 10:56 AM

08.11.2024 10:56 AMA deep-seated fear of a return to prolonged deflation looms within Japanese society—a challenge that both the government and the Bank of Japan have struggled to overcome for decades. The idea of postponing a rate hike by the BOJ until at least the spring of next year is gaining traction. Recent proponents of this pause include BOJ board member Adachi, Yuichiro Tamaki (leader of the increasingly popular Democratic Party for the People, which quadrupled its representation in the lower house elections on October 27), and other influential figures.

The reasoning is straightforward: wage increases in the spring of 2024 were a significant factor in the BOJ's decision to begin exiting its negative interest rate policy. However, there's no guarantee that similar wage growth will occur in the spring of 2025. Observers argue that waiting for the outcome is prudent before considering another rate hike. This year's wage growth has been the highest since 1997, yet real household incomes continue to fall due to high inflation—declining by 1.9% year-over-year in August. Raising rates amid falling real incomes could severely impact consumption, GDP, and overall spending, potentially ushering in deflation—or worse, stagflation, a nightmare scenario for any government.

Such an approach is unlikely to support yen appreciation, especially as the Federal Reserve's policy recalibration gains attention following Trump's victory. Yesterday, the FOMC predictably cut rates by a quarter point, and futures now project only four additional cuts through the end of 2025, bringing the rate to 4%. This indicates a strong dollar, aligning with Trump's campaign rhetoric favoring a robust U.S. currency, which signals higher yields.

The markets will likely remain volatile in the near term, with headline-making announcements and personnel changes adding to the turbulence. However, the yen's prospects look weak. The factors that fueled its remarkable strength from July to September are no longer in play.

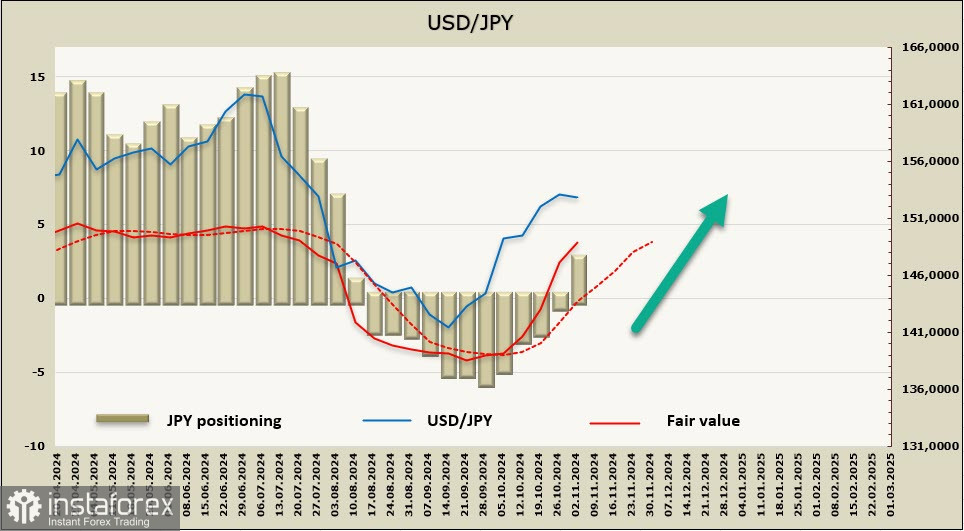

The yen maintained a bullish bias for just 11 weeks. As of the latest reporting period, this phase has ended, with a weekly change of -$3.1 billion, leading to a net short position of $2.0 billion. The yen and the euro are now competing in terms of sell-off momentum, with both currencies currently appearing weak against the dollar.

Last week, we anticipated sustained yen depreciation, which materialized. Following the announcement of the U.S. presidential election results, USD/JPY surged to 154.71, with only a shallow pullback afterward. Realistically, few reasons exist to expect a reversal in the yen's trajectory. The likely scenario is continued growth toward the multi-year high 161.79, set in July. The only potential obstacle to this upward trend would be an unexpected surge in demand for safe-haven assets—an unlikely scenario in the current environment.

You have already liked this post today

*यहां पर लिखा गया बाजार विश्लेषण आपकी जागरूकता बढ़ाने के लिए किया है, लेकिन व्यापार करने के लिए निर्देश देने के लिए नहीं |